🏠🛡️ HO3 vs. HO5: Is Your “Standard” Policy Leaving You Exposed?

Following up on my last post about the “secret codes” at the bottom of your policy, the most common designation you’ll see is HO3. But the one you may actually want is HO5.

The difference in how these two policies handle a claim can be massive. Here’s the breakdown.

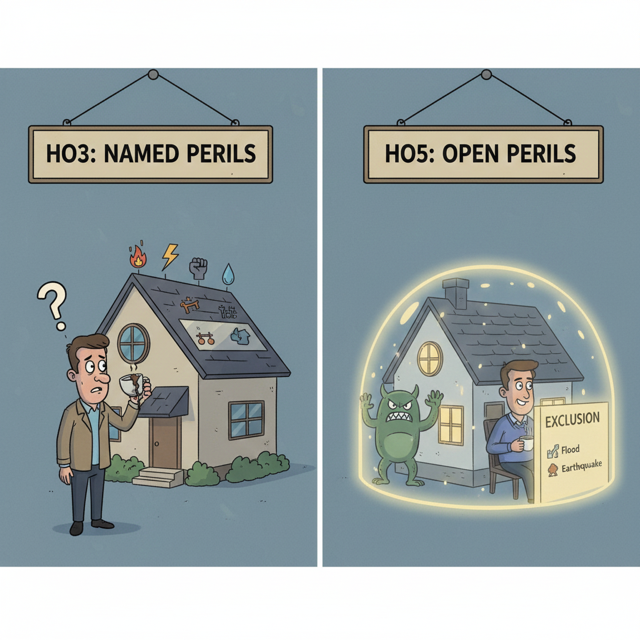

🏡 The HO3: The “Special Form”

The HO3 is the industry standard. It uses a hybrid approach to coverage:

- Your House:

Covered for everything unless specifically excluded (such as flood or earthquake). - Your Stuff:

Personal property is only covered for Named Perils.

That means you must prove your loss was caused by one of 16 specific events—like fire, theft, or wind.

If the cause of damage isn’t on that list, there is no coverage.

🛡️ The HO5: The “Comprehensive Form”

The HO5 is considered the gold standard of homeowners insurance.

It provides Open Peril coverage for both:

- the structure and

- your personal property

- The Benefit:

Instead of you proving what caused the damage, the insurance company must prove the loss was excluded. - The Advantage:

HO5 policies cover accidental losses that HO3 policies typically deny—such as spilling wine on an expensive rug or losing a wedding ring.

⚠️ Why This Matters

Many homeowners assume “everything is covered” until they file a claim for a strange or accidental loss—and receive a denial because it wasn’t a Named Peril.

Upgrading to an HO5 is often surprisingly affordable, yet it dramatically shifts the burden of proof away from you and onto the insurance company.

Take Action

Look at the bottom-left corner of your policy today.

Does it say HO3… or HO5?

That single line of text could determine how well protected you really are.