📺💸 ACV vs. RCV: Will Your Insurance Payout Actually Cover a New TV?

The final piece of the “policy code” puzzle is how your insurance company calculates your check after a loss.

You’ll usually see one of two terms in your policy:

- Actual Cash Value (ACV)

- Replacement Cost Value (RCV)

The difference between them comes down to one word:

Depreciation.

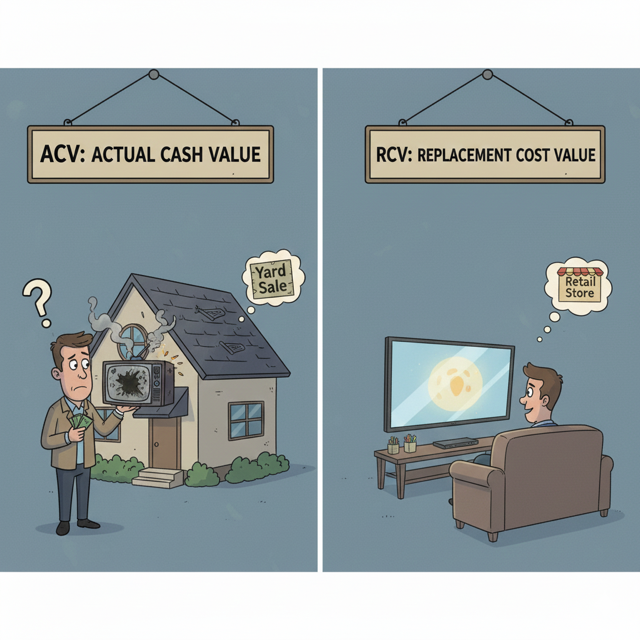

🏷️ Actual Cash Value (ACV): “The Yard Sale Price”

ACV pays you what your items were worth at the moment they were destroyed.

- The Math:

Replacement Cost minus depreciation (age, wear, and tear) - The Reality:

If your five-year-old laptop is stolen, ACV won’t give you enough to buy a new one.

It pays what that used laptop would sell for on eBay today.

In most cases, that’s far less than what it costs to replace it.

🛒 Replacement Cost Value (RCV): “The Retail Price”

RCV is the gold standard for most homeowners and property owners.

It ignores how old your belongings are.

- The Math:

Whatever it costs to buy the item brand-new today (of like kind and quality) - The Reality:

If that same five-year-old laptop is stolen, RCV provides enough money to walk into a store and buy the modern equivalent—with no deductions for age.

⚠️ Why This Matters

Many “standard” policies default to ACV for personal belongings to keep premiums low.

But in a major loss, the gap between used value and replacement cost can easily be tens of thousands of dollars—paid directly out of your pocket.

The Advice

Review your policy’s Loss Settlement provisions carefully.

Upgrading your personal property coverage to Replacement Cost Value is often one of the **most impactful—and surprisingly affordable—**improvements you can make to an insurance policy.

When disaster strikes, the right valuation method makes all the difference.