The headlines today from the Wall Street Journal and the California Department of Insurance are a sobering wake-up call for policyholders. California is "throwing the book" at State Farm, seeking millions in penalties and even a potential license suspension over the "mishandling" of claims from last year’s wildfires.

According to state investigators, the issues weren't just administrative. They found a pattern of:

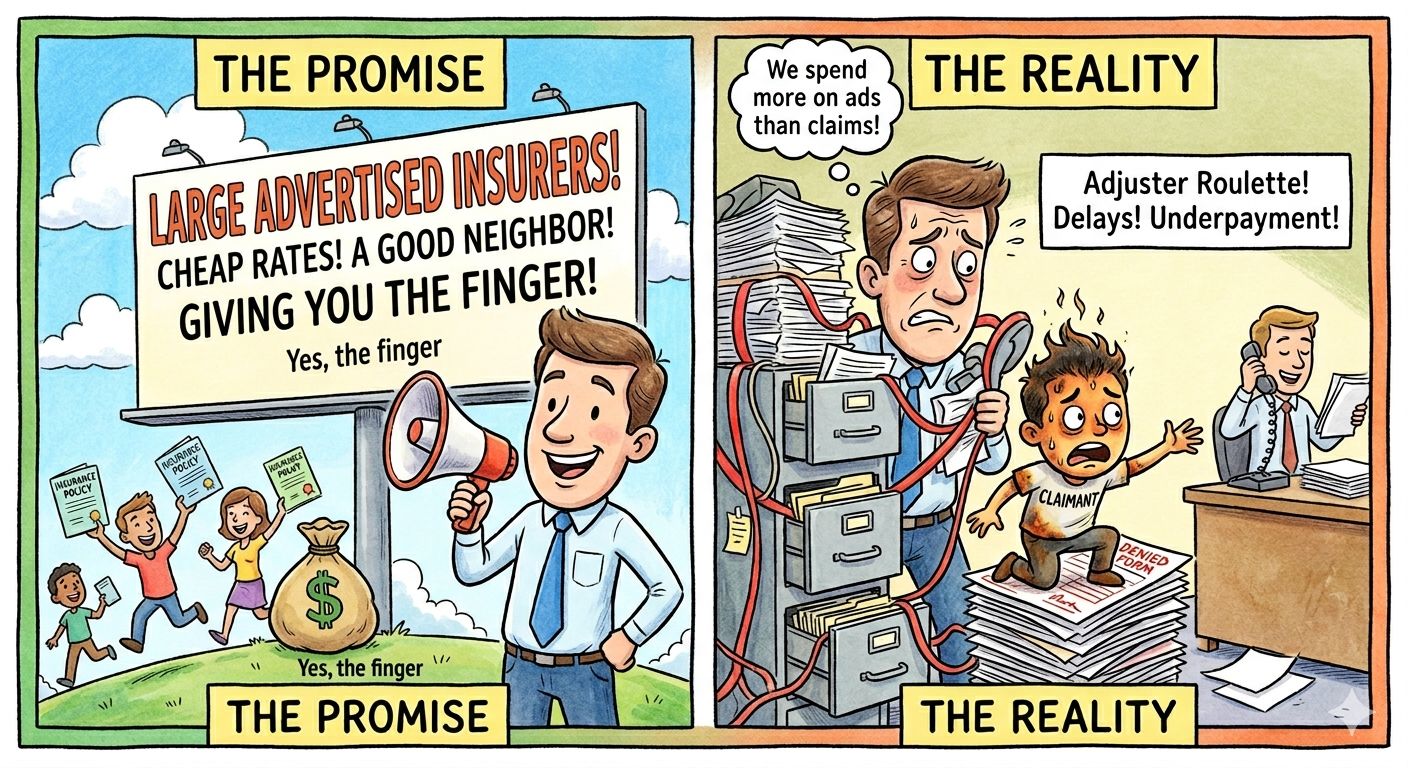

• "Adjuster Roulette": Shuffling policyholders between dozens of different adjusters.

• Unreasonable Delays: Failing to investigate or pay claims within legal timelines.

• Underpayment: Making low settlement offers and burying survivors in red tape.

The Advertising Trap

As someone who handles insurance claims every single day, I have a general rule: If a company spends more time advertising their "low prices" and "good neighbor" status than they do training their adjusters, stay away.

When you see a carrier's logo on every stadium, billboard, and commercial break, remember that those billions of dollars are coming from somewhere. Too often, they aren't going back to the policyholders when disaster strikes. In fact, many of the calls I get are from people who thought they were "in good hands" until they actually had to file a claim.

The "Gamble" of Large Carriers

People often choose these massive carriers because they are household names. But as we are seeing in California, being "large" often just means there is more red tape to hide behind. You might save a few dollars on your monthly premium, but you’re essentially gambling that you’ll never have a major loss.

If you do have a loss, you’ll find that your money was better spent elsewhere—or even saved in a bank—rather than being paid to a company that treats your recovery like a line item to be minimized.

My Advice: Look Beyond the Billboard

Don’t wait until your house is gone or your business is underwater to find out if your carrier is actually a "good" company.

1. Ask around: Talk to people who have actually had large claims settled.

2. Check the "Market Conduct" history: States like California investigate these patterns for a reason.

3. Prioritize Service over Savings: A cheap policy is the most expensive thing you’ll ever buy if it doesn't pay out when you need it.

If you’re currently battling one of these "advertised" giants and getting nowhere, don't keep banging your head against the wall. The "red tape" is designed to make you quit.

Have you had a claim experience with a "Big Box" insurer that didn't live up to the commercials? Let’s discuss in the comments.